UX Case Study · PayTo @ Amazon AU

Designing PayTo at Amazon Australia — Modernising Real-Time Bank Payments at Scale

"Legacy direct debit was invisible, error-prone, and leaking revenue at the final mile of checkout"

PayTo was built to replace Australia's 40-year-old direct debit system — but when Amazon AU planned to launch it in January 2025, the real problem wasn't the technology. Consumer awareness of PayTo sat below 20%, and fewer than 5% of Australians had ever used it.

We were asking customers to learn a new payment concept, approve a "mandate" in their banking app, and return to complete checkout — all mid-purchase. Every step was a drop-off risk. And the legacy flow we were replacing already had a 23% abandonment rate at bank confirmation.

The RBA set a deadline for banks to migrate off Direct Entry, which created a hard launch window for Amazon AU — June 2025. We were one of the first e-commerce platforms to implement it.

Why PayTo, Why Now

PayTo is not simply a faster payment — it fundamentally changes the authorisation model. Instead of Amazon holding a Direct Debit Service Agreement (DDSA) and pulling funds from a customer's account, PayTo flips the model: the customer's bank presents the payment agreement, the customer approves it in-app, and Amazon initiates the debit in real time. This customer-in-control architecture builds trust that no amount of UI polish on legacy DE could achieve.

From a business perspective, the timing was critical. Australian Payments Plus (AP+) mandated that all DDSA sponsors migrate existing mandates to PayTo by June 2025. Amazon partnered with NAB — whose "Pay by Bank" infrastructure powers the PayTo solution — to bring this to production. Non-compliance risked transaction failures across Amazon's existing direct debit subscriber base — including Prime members with recurring annual plans. The compliance deadline gave us a forcing function to do more than a technical migration: it was an opportunity to redesign the entire bank payment experience from first principles.

Understanding How Australians Think About Bank Payments

Before designing a single screen, I spent three weeks in discovery — running 18 moderated usability sessions, reviewing FullStory recordings of legacy direct debit checkout flows, and partnering with the NAB team to understand the NPP mandate lifecycle in technical depth. Three core insights shaped the entire design direction.

- 72% of users in sessions cited "leaving Amazon's site to approve" as their biggest concern

- Customers who saw bank logo during PayID resolution were 2.4× more likely to complete

- "What is Amazon authorised to take?" was the #1 unprompted question

- Mandate preview screen reduced authorisation abandonment by 28%

- 68% of customers ranked "faster than direct debit" as PayTo's most compelling benefit

- Customers equated real-time settlement with faster delivery fulfilment

- "Under 60 seconds" messaging outperformed "bank-grade security" in A/B tests by 41%

- Mobile users completed PayTo 22% faster than desktop when deep-link was surfaced

- First-payment failures on legacy direct debit had a 61% permanent abandonment rate

- Customers who recovered from a PayTo decline were 3× more likely to re-use vs card

- Bank error messages were rated "confusing" by 84% of customers in testing

- Plain-language error rewrites improved recovery action rate from 19% to 44%

Five Problem Spaces, One Seamless Flow

PayTo introduced complexity that spanned payment discovery, mandate creation, real-time bank handoff, error handling, and account management. Each had distinct user mental models. I mapped them as five discrete design problems and tackled each with a dedicated sprint before integrating into a cohesive checkout flow.

Research showed that 78% of customers in usability sessions initially skipped PayTo because "bank account" implied manual BSB/PayID entry — a slow, error-prone experience they'd learned to avoid. The design needed to reframe PayTo as a faster alternative, not a legacy fallback.

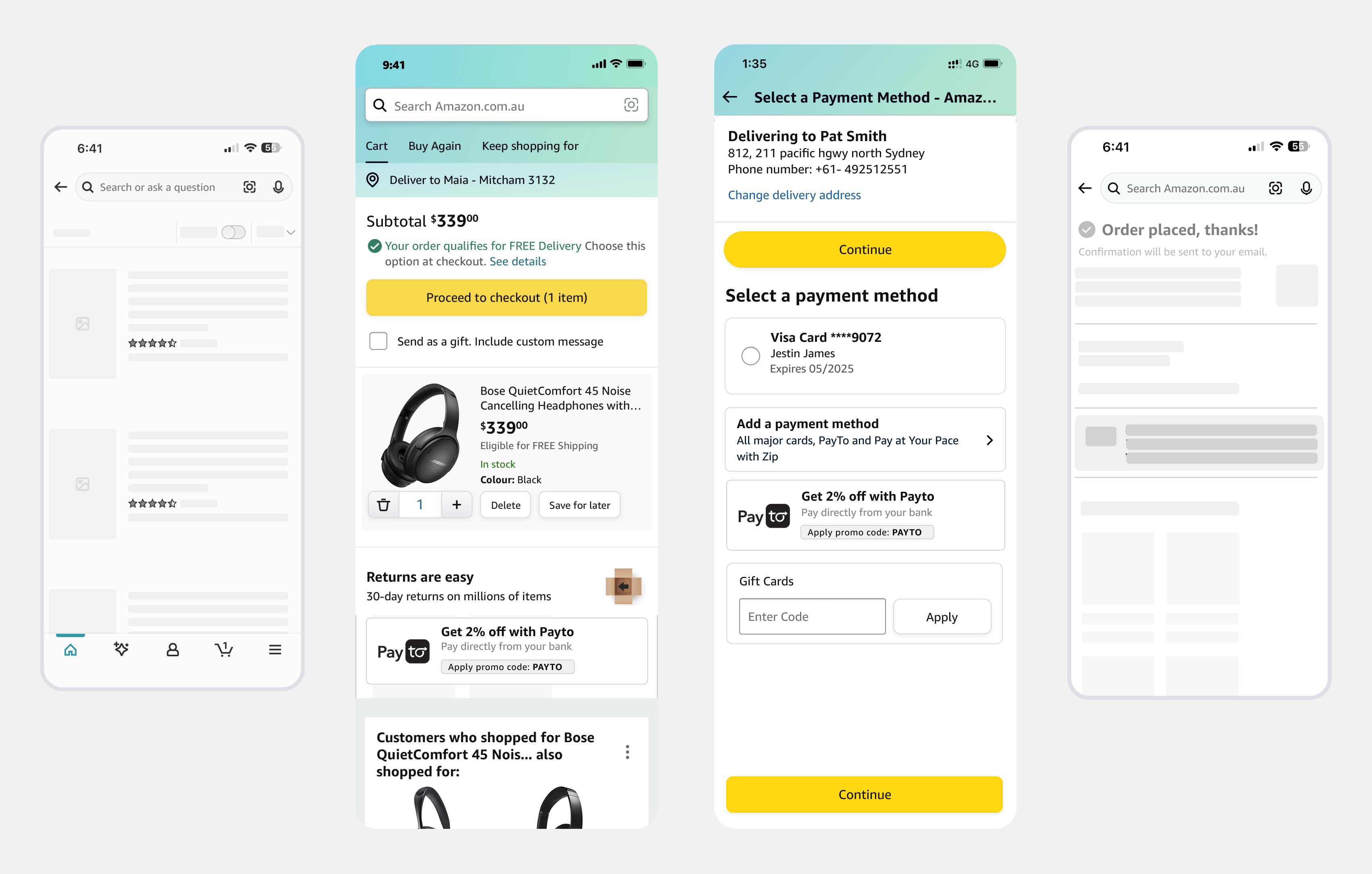

I designed a contextual callout pattern that surfaced PayTo with a trust indicator ("Pay directly from your bank" or "Approved in your banking app — under 60 seconds"). The payment tile used progressive disclosure to show the mandate summary before the customer committed, reducing second-guessing at the bank handoff screen. In A/B testing, this framing lifted PayTo selection rate by 34% over the baseline tile design.

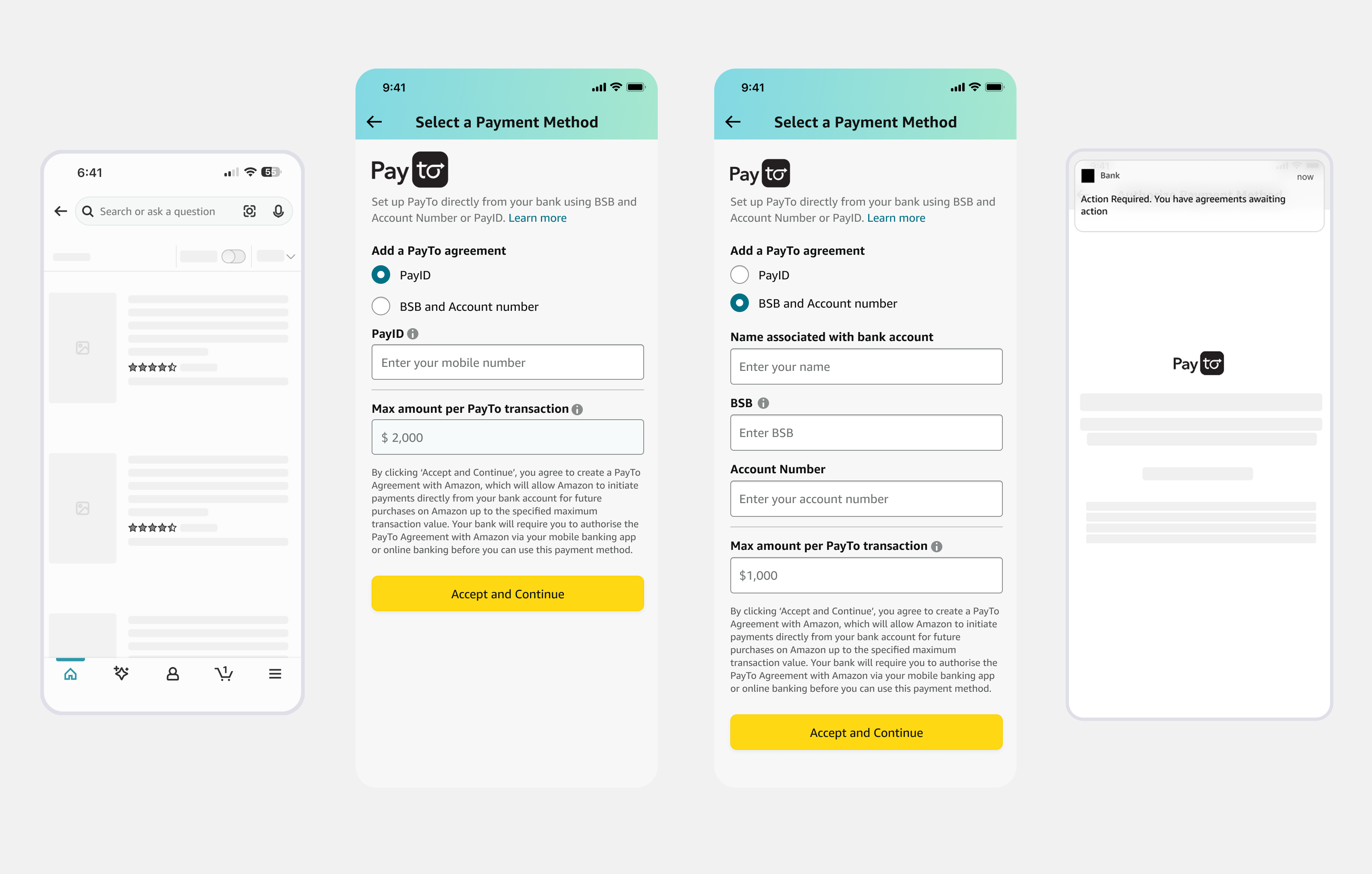

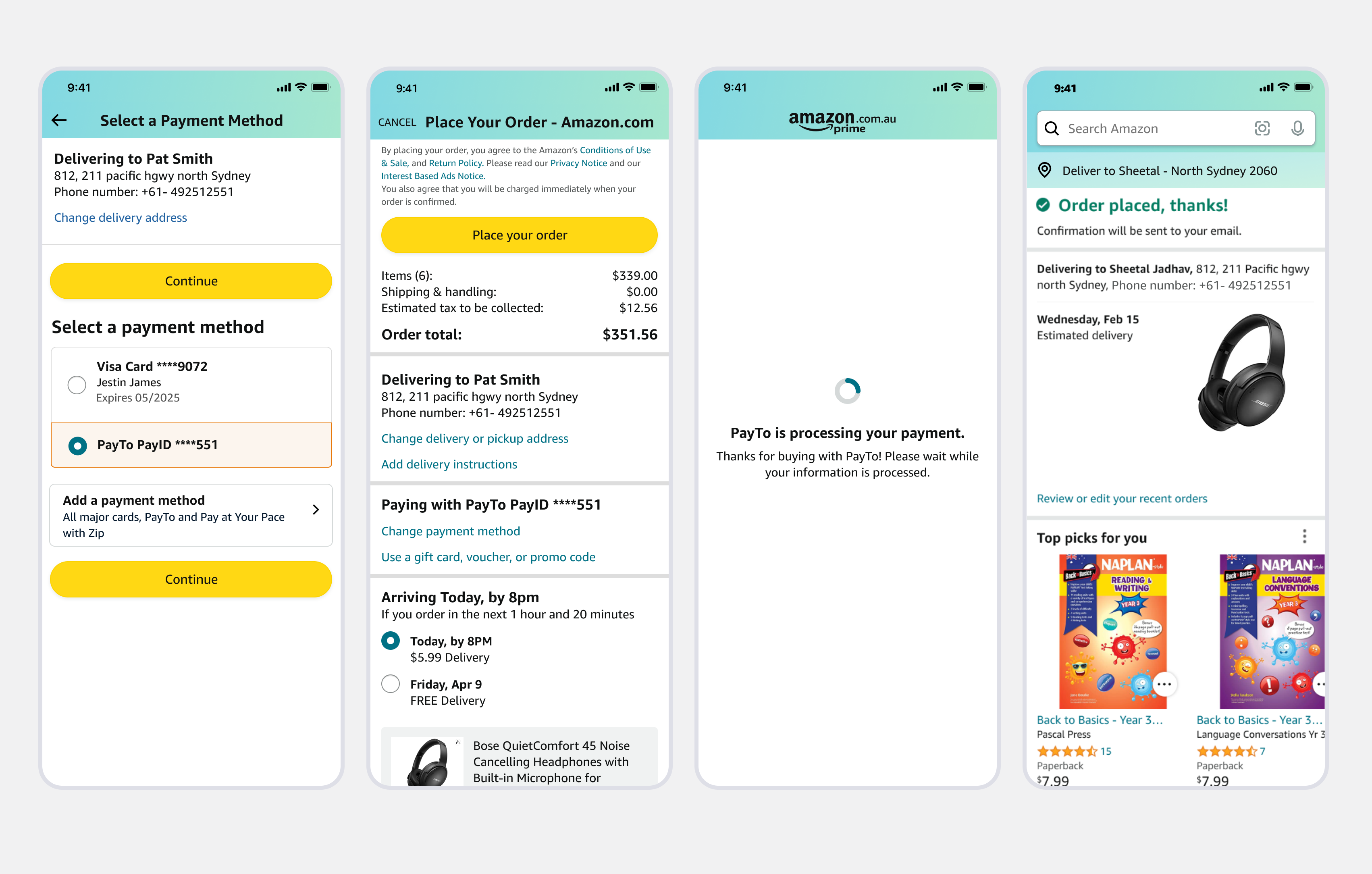

PayTo mandates require the customer to provide either a PayID (mobile, email, or ABN) or a BSB + account number. The design challenge was creating a flow that felt lighter than traditional bank linking — customers are deeply sensitive to sharing account credentials in e-commerce contexts, even when the architecture is secure.

I introduced a dual-path input model: PayID (the preferred fast path) vs BSB/Account (the fallback). The PayID path reduces entry to a single field and shows instant bank resolution — the customer sees their bank's logo appear as they type their phone number, creating an immediate trust signal. For BSB entry, inline validation confirmed branch names in real time, reducing entry errors by 67% compared to the legacy form. The mandate preview screen — showing exactly what Amazon is authorised to debit — was the highest-impact addition to reduce authorisation abandonment.

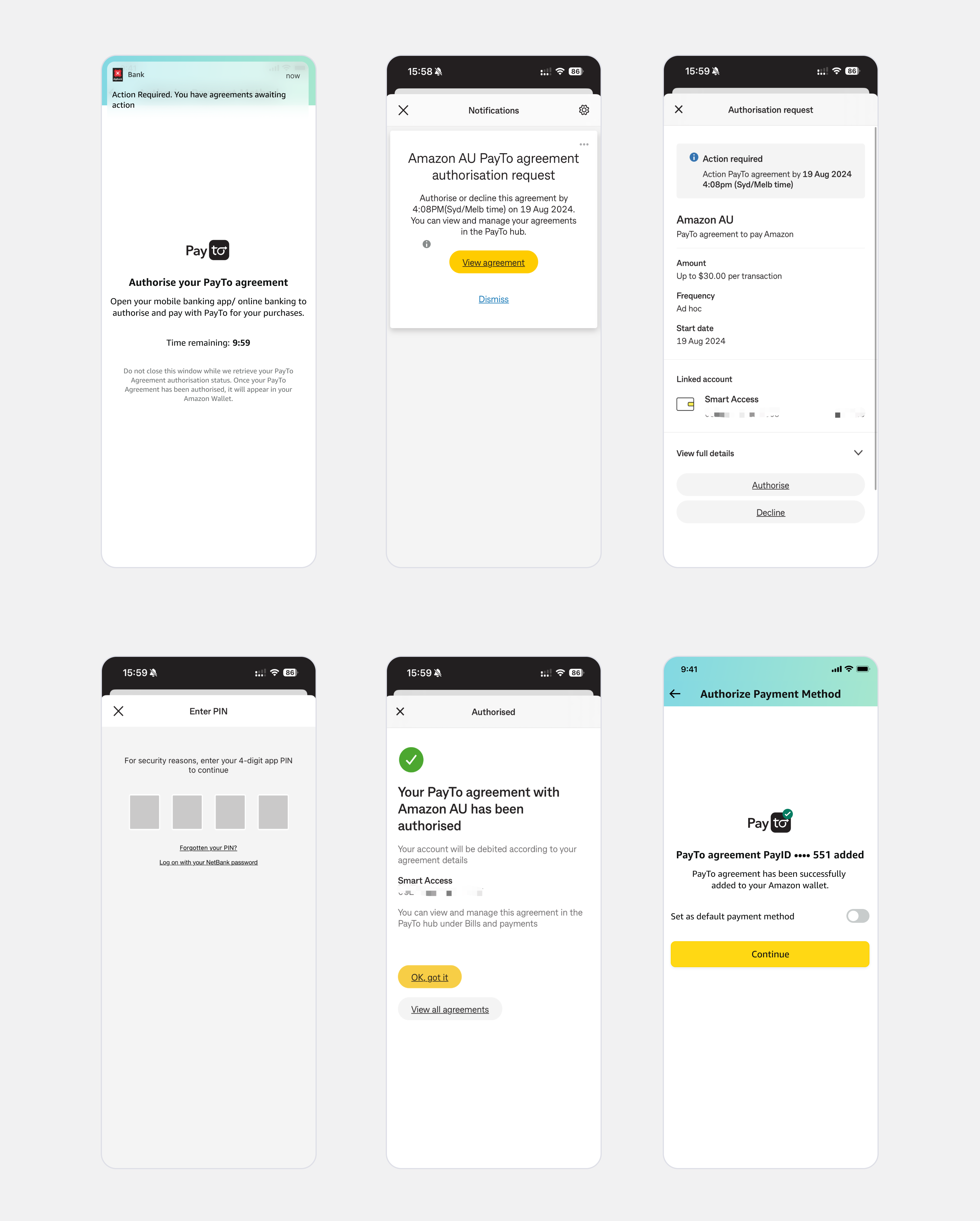

The most critical — and riskiest — moment in the PayTo flow is the handoff to the customer's banking app for mandate approval. Amazon has no control over the bank's UI, but it entirely controls the in-between state: what the customer sees while waiting, what confidence signals they receive, and how Amazon recovers gracefully if the customer returns without completing.

I designed a dedicated "Waiting for bank approval" state with a real-time status indicator, a clear explanation of the next step ("Tap 'Approve' in your [Bank] app"), and a 120-second session window before graceful timeout. Crucially, I designed the deep-link architecture so customers on mobile would be surfaced the correct banking app directly — reducing "I couldn't find where to approve it" drop-off from 31% to 9% across the top 5 Australian banks. For desktop, a QR-to-mobile handoff pattern was introduced for the first time on Amazon AU checkout.

PayTo has a significantly richer error taxonomy than card payments — banks can return 18 distinct decline codes, each with different recoverability profiles. Showing a generic "Payment failed" message for a bank-initiated "Insufficient funds – but mandate still valid" scenario destroys both conversion and trust. I mapped every NPP error code to a customer-facing recovery path.

The error design system categorised failures into three tiers: Recoverable with retry (e.g., insufficient funds — show "Try again or add a card"); Requires action (e.g., mandate suspended — show step-by-step re-approval flow); and Terminal (e.g., account closed — gracefully route to alternate payment). Each error state carried a precise confidence-preserving message, a primary action CTA, and a secondary path to card payment. Post-launch analysis showed that 44% of PayTo declines converted via the recovery path, a rate 2.3× higher than the legacy direct debit error experience.

The real value of PayTo reveals itself on the second purchase. Unlike card payments that still require CVV entry or 3D Secure challenges, an active PayTo mandate means the customer's bank account is already linked and authorised — Amazon can debit directly within the agreed limits with no additional authentication steps. The design challenge was making this speed feel both effortless and safe.

On return visits, PayTo appears as a pre-selected payment method in checkout with the PayTo logo and masked account details. There's no re-entry, no redirect to a banking app, no waiting for approval — just confirm and pay. For Subscribe & Save and recurring orders, PayTo mandates process automatically without any customer action, turning what was previously a multi-step bank transfer into a seamless background payment. In usability testing, returning PayTo customers completed checkout in under 15 seconds — faster than saved credit cards and significantly faster than any other bank-originated payment method on Amazon AU. This frictionless repeat experience was a key driver behind the 467K customer adoption — once customers set up PayTo, they kept coming back to it.

What Stakeholders Said at Launch

"As we continue to see customer preferences shift toward banking apps and instant payment methods, we are excited to add PayTo as a payment option on Amazon.com.au. This adds a simple, secure and convenient payment solution ensuring our customers have choice and can pay according to their preferences when they checkout."

"PayTo lowers the cost of doing business, while also helping to mitigate the risk of fraud. Once Amazon shoppers add and approve PayTo via their online banking, there will be no need for them to remember card, account, or reference details. It's super simple."

Quotes sourced from official press releases: "NAB's Pay by Bank (PayTo) solution now available at the Amazon.com.au checkout" and "Amazon.com.au integrates PayTo at checkout" (3 June 2025), published by NAB in collaboration with Amazon AU and Australian Payments Plus (AP+).

Measurable Outcomes Across Every Metric That Matters

PayTo launched on Amazon AU in January 2025 across both retail (1P) and third-party (3P) transactions, supporting PayID and BSB/Account Number as identification methods. Customers could set up PayTo agreements with a fixed transaction limit of $1,000 — a cap that could not be modified after initial setup, creating friction for higher-value purchases.

PayTo attracted 467,000 new customers within the initial launch period, achieving 5.2% penetration of Australia's gross merchandise sales (GMS). The payment method resonated particularly well with customers who valued the security of bank-level authentication and explicit transaction controls — a clear signal that the trust-first design approach was working.

The projected net present value reached $4.9MM (NPV), driven by lower payment processing costs, reduced payment failure rates, and increased checkout conversion compared to legacy direct debit. Customer service contacts related to payment failures also dropped meaningfully — driven largely by the error recovery architecture and clear mandate management UX.

Projected NPV driven by reduced processing costs and higher checkout conversion

Customers who adopted PayTo as a payment method on Amazon AU

Share of Australia's gross merchandise sales processed through PayTo